“The Hidden Power” Big Tech´s Foray into Financial Services: A Significant Shift?

Picture Source: IT Capital original -Big Tech´s Foray into Financial Services: A Significant Shift?

Research Article Appro. (June 10th, 2025). Big Tech’s Foray into Financial Services: A Significant Shift?

Abstract

The period between 2010 and the present has been marked by a significant and transformative entry of major technology companies—known as Apple, Google (Alphabet), Meta, Amazon, Microsoft, Alibaba, among others, collectively referred to as “Big Tech”—into financial services ecosystems, historically dominated by regulated banks and various public and private market financial institutions.

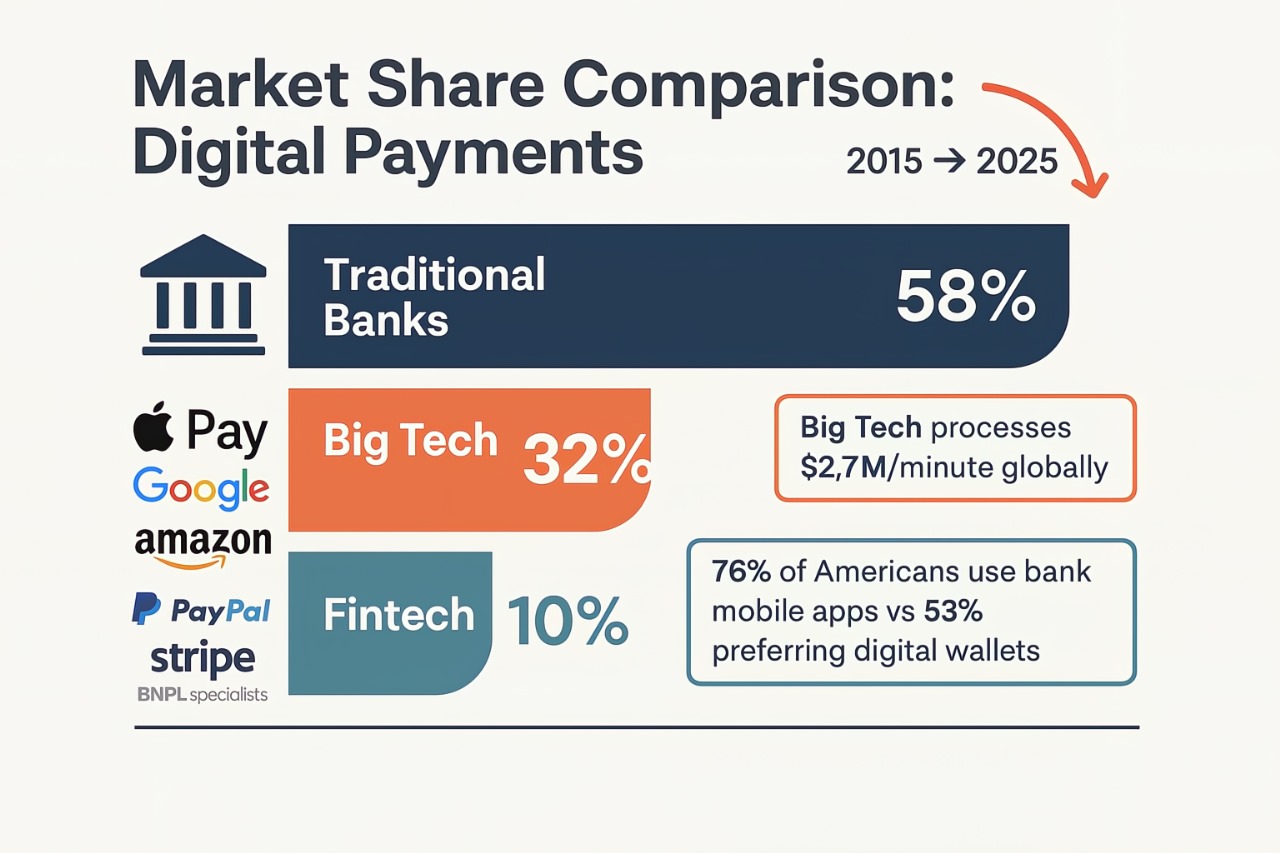

Introduction A) User Base Comparison

The traditional banking environment has been significantly transformed by the integration of financial services within the ecosystems of Big Tech companies. These tech giants leverage their vast user bases (with an estimated total of ~17.228 billion users in 2025 across the top 25), their advanced data analytics capabilities, and their technological infrastructure to offer financial products and services. This poses a direct challenge to the top 25 global banks, which have an estimated ~4.024 billion users in 2025, as well as to other financial institutions, including the top 25 digital banks and alternative financial entities, with a combined user base of approximately ~800 million in 2025.

Market Penetration Metrics

⦿ Digital Payments: Big Tech controls approximately 32% of the global digital payments market, with projections to reach 40% by 2027.

Future Strategies (2025–2030)

⦿ Banking Licenses: Amazon or Apple could acquire ILC (Industrial Loan Company) licenses to reduce their reliance on financial partners.

⦿ Integration with Central Bank Digital Currencies (CBDCs): Big Tech would act as distribution partners for digital dollars or euros.

⦿ AI-driven Banks: Microsoft or Google could launch autonomous banks powered by generative and agentive AI.

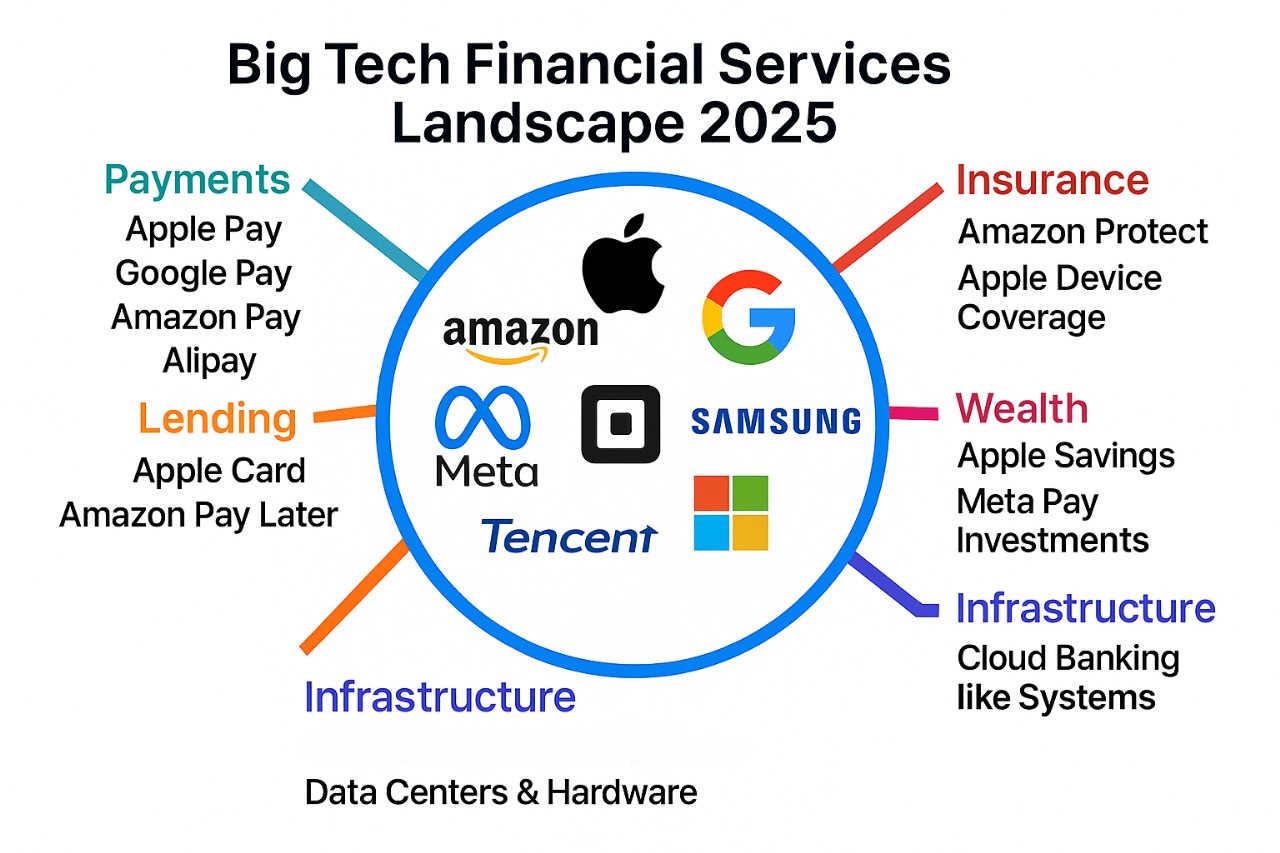

Financial Technology and the Legal Grey Zone Includes:

⦿ Digital Payments and Wallets (Apple Pay, Google Pay, Amazon Pay)

⦿ Consumer Lending (Buy Now, Pay Later through Apple, Amazon, Meta)

⦿ Customer Data Monetization (Profiling and behavioral segmentation without banking-equivalent protections)

⦿ Predictive Models / Behavioral Profiling (Creation of personalized financial and business risk models through AI, LLMs, ML, and other predictive tools)

Expert Conclusions

Experts highlight both opportunities and risks associated with Big Tech’s entry into financial services:

⦿ Innovation: Their technological capabilities can drive innovation and improve financial inclusion.

⦿ Systemic Risk: Their size and interconnectedness could pose risks to financial stability.

⦿ Regulatory Challenges: Existing financial regulations may be insufficient to address the unique risks posed by tech-driven financial services.

A balanced approach is required to harness the benefits while mitigating potential risks.

A) The Oligopoly Imperative

Big Tech companies employ strategies characteristic of oligopolies, as noted by experts in economics and finance:

⦿ Market Power: Their massive user bases—numbering in the billions—and their control over consumption and other behavioral data allow them to influence market trends and consumer behavior, fostering loyalty through automated and hyper-personalized processes.

⦿ Vertical Integration: By controlling hardware, software, and services, they create closed ecosystems within their platforms, devices, and technological environments.

⦿ Network Effects: The value of their services increases as more users join, creating high entry barriers for new competitors.

B) Although innovation

(for example, financial inclusion in developing countries) is real, systemic risks demand a reassessment of antitrust frameworks in the digital age to prevent the collapse of traditional financial ecosystems.

As Bjorn Cumps (Vlerick Business School) warns:

«Today’s convenience may become tomorrow’s dependency. We must ask ourselves: Who holds the keys to the financial system?»

Press and Research References (Sources & Articles):

1. Big Tech in Financial Services. Congress.gov (congress.gov)

2. Alibaba Group Announces March Quarter 2025 and Fiscal Year 2025 Results. Business Wire. (businesswire.com)alibabagroup.com

3. Ant Group. Wikipedia. (en.wikipedia.org) businesswire.com And…… 60 more.

This is a completely free research article, produced by a non-profit association for informational purposes only. Its distribution is authorized exclusively by IT Capital. Any other use is not authorized by IT Capital or its authors.

")